")

MicroStockHub

Introduction

The equity REIT sector has had a strong showing lately. Many even believe that a big REIT recovery has begun. A natural question becomes how the situation is with mortgage real estate investment trusts (mREITs). Will they also participate in the rally? TPG RE Finance Trust (NYSE:TRTX) seems to provide a very positive answer. The small-cap sized mREIT demonstrated a price strength in July, which has been up by 11%. Considering that the dividends paid by mREITs are higher than equity REITs, it is a good time for income investors to build mREIT wealth portfolio with quality mREITs, like TRTX, which provides a 10% dividend. The rate-cut may induce a reversion to the normal yield curve, which will be a big catalyst for the mortgage market. TRTX is expected to be a winner under such conditions. Its stock price may be further driven up by the small-cap rotation, which is also gaining quite some momentum lately.

TRTX Portfolio Highlights

TRTX is a mortgage real estate investment trust (mREIT), managed by TPG, a Global Asset Manager.

Its loan portfolio has the following breakdown, as shown below:

- Multifamily: 50%

- Office: 20.4%

- Life Sciences: 11.4%

- Hotel: 9.9%

Notice that in 2023, the management had actively reduced the more risky exposures to Office loans and increased more Multifamily exposures. A more favorite balance point seemed to be reached at the end of Q1 in 2024. The latest breakdown in the loan portfolio from Q1 shows management’s confidence in the loans going forward. In fact, its CFO pointed out in the Q1 earnings conference call that “Our loan portfolio is 100% performing“.

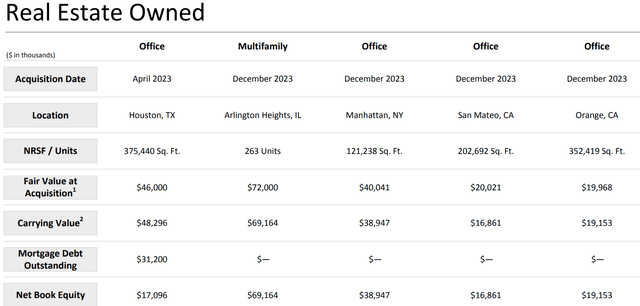

It is interesting to note that TRTX owns the real estate assets, which are mainly divided into Multifamily and Office, as shown below. The geolocations are in the areas with population growth. Therefore, TRTX is expected to illustrate REIT characteristics to a certain extent.

TRTX Real Estate Assets – from TRTX investor presentation

The following summarizes some key market characteristics for TRTX:

- Market Cap: $752.61M. It is a small-cap stock.

- Volume (last day): 2,141,039. It is a relatively high volume, given its size.

- Tangible Book Value (3-Y average): -4.26%. The decreased book value has been impacted mainly by the rapid rate hiking in 2022-2023. However, compared to the 5-year average at -4.93%, TRTX has held its book value up well more recently.

- Yield: 10.23%. The double-digit dividend is appealing to income investors.

- Payout Ratio: -29.45%. It is a high risk for dividend cut. TRTX appears to be in a need for favorite yield spread more urgently than the other mREITs with positive payouts.

Small-cap mREIT benefits from Small-Cap market rotation

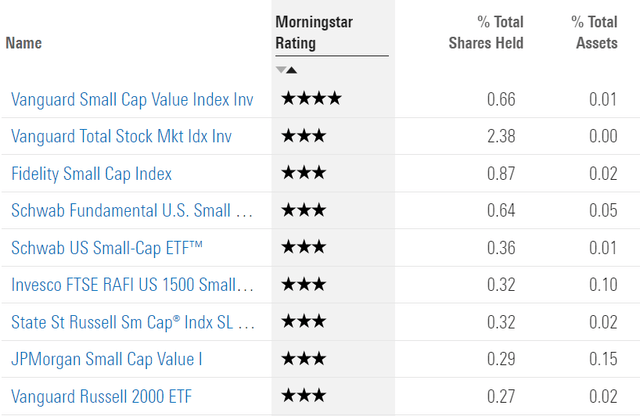

The small-cap nature of TRTX has been noticed by the market. TRTX has been selected as a holding by some well-known benchmark indices and funds, including Vanguard, Fidelity, Schwab, and JPMorgan, as shown below:

TRTX owners – from morningstar.com

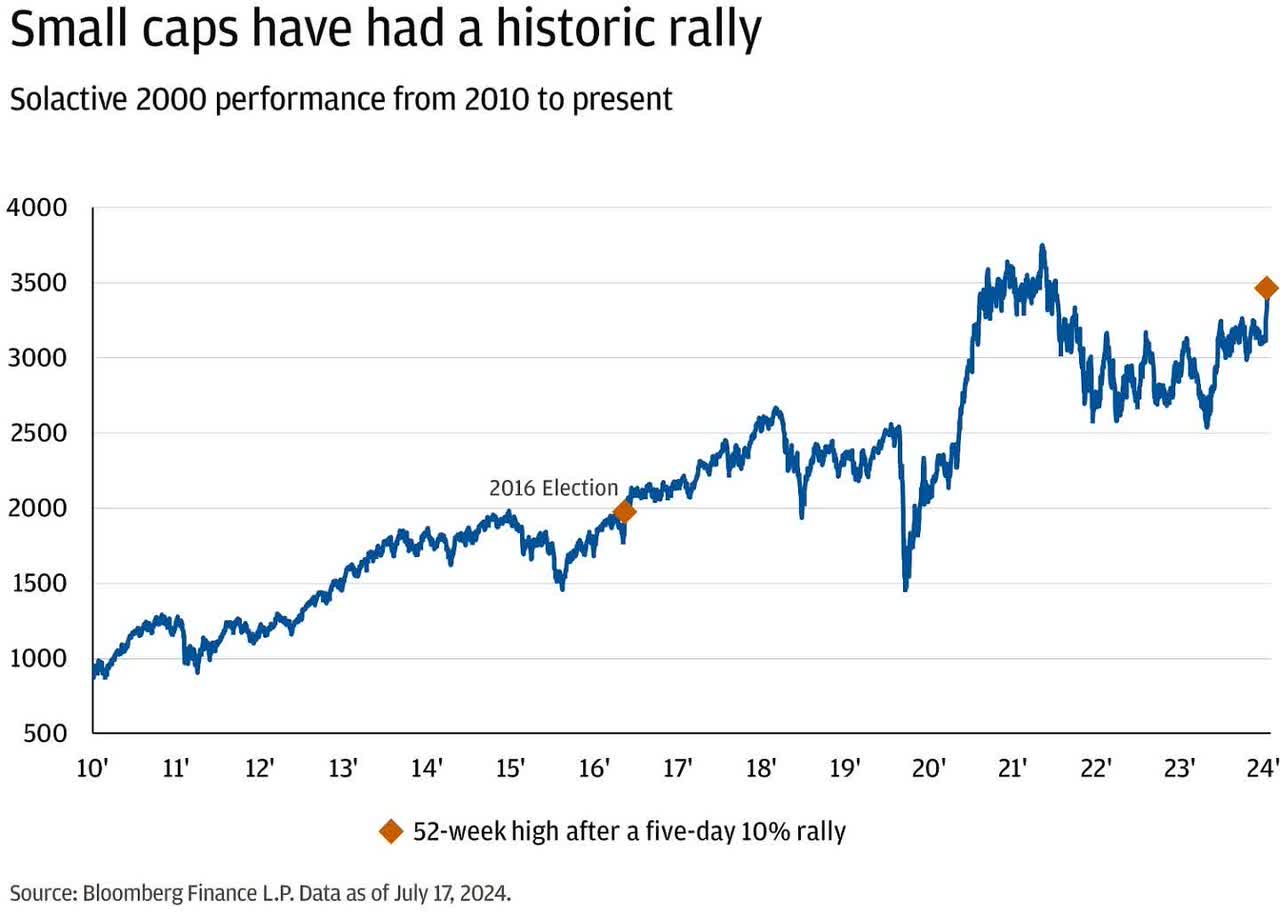

The small-cap stocks have had a nice rally recently. As shown below, some even called it “a historical rally” just two days ago:

Small Cap Rally – from Bloomberg

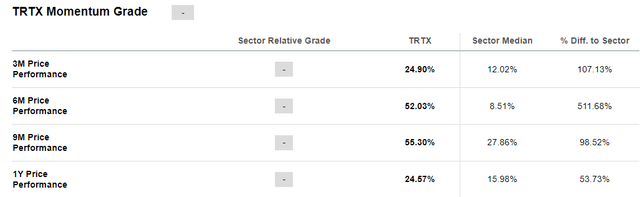

At the same time, TRTX’s stock price itself has also staged a remarkable rally, which has uplifted many of its performance metrics. For example, Seeking Alpha has shown a set of very impressive momentum numbers for TRTX, although ratings have not yet been provided, as shown below:

TRTX Momentum – from SA database

Looking ahead, there will be more than one tailwind (small-cap rotation) that will be driving the TRTX’s price momentum forward. The following provides a list of opportunities based on my observations:

- Small-Cap market rotation started in July. TRTX’s small-cap size and the constituent status in small-cap indexing funds have helped to attract money to flow into its stock. I believe that the rotation will continue in the months to come.

- There is also value rotation that is relatively quieter but in progress. TRTX with its low price-to-book ratio will become a winner, if the value rotation continues to go with a bigger swing.

- REIT recovery will continue to unfold as a process to achieve its NAV-reverting restoration. TRTX and mREIT as a whole are expected to go along with it.

The improving yield curve is positive to mortgage

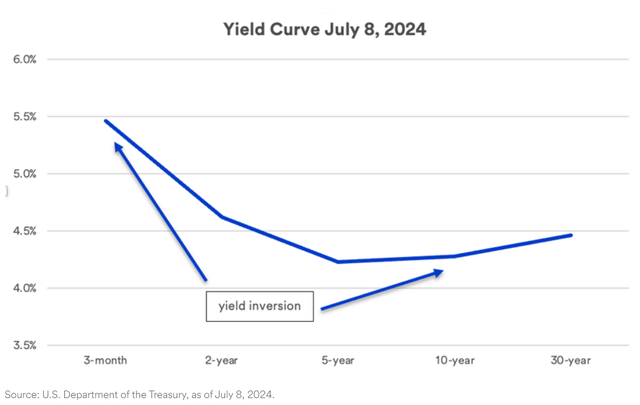

Rate-cut could be a tailwind for the mREIT from the perspective of mortgage loans. The direct impact actually comes from the yield curve. Declining interest rate will help to reverse the inverted yield curve, and this will help mortgages gain more profit. Although the current yield curve is still inverted, there are signs to suggest that inversion is improving, as indicated by an article from USBank.com, “The inversion today is flatter than it was during periods in 2023. For example, yields on 10-year and 30-year securities now exceed those of 5-year Treasuries.“

The following Yield Curve illustrates that there is still quite some room for the yield inversion to be improved and eventually corrected at some point of time in the future. Therefore, my bullish view is that it is the reverting process of yields that will help to drive up the mREIT stock price in the market.

Yield Curve – from the chart used in USbank.com

Wise Core Grower for income WWE portfolio

Given that the yield curve is still inverted, I believe it is wise to adopt a more conservative approach in establishing the mREIT wealth engine within the income portfolio.

The following is a refresher of the WWE from my previous article:

- The key idea of WWE is to use distribution income to feed into a core growth engine of the portfolio.

- There is a growth bias to select the holdings for Core Engine, which form the main driver for long-term capital appreciation.

- There are many Capturers used to collect the dividend. The capturers are often offering double-digit yield or among the ones that offer the highest dividends in a target group (e.g., a sector).

I plan to use TRTX as the growth Core Engine and the income Capturer. There will only be allocation for the income part and the Core will be built from the income streams (distribution), which include the reinvestment of TRTX’s dividend itself. This follows the conservative bias mentioned above. As a result, the core part will be built rather slowly and gradually.

The target group is mREIT with the following mREIT stocks considered at the moment. Please view this as another showcase for WWE.

#1 TRTX. It is recommended as Core Engine and Capturer. (TRTX’s details are given in the earlier section).

#2 AGNC Investment Corp. (AGNC). AGNC is “THE PREMIER AGENCY RESIDENTIAL MORTGAGE REIT” and one of the largest mREIT. Its higher dividend makes it a good fit as a WWE income Capturer.

- Market Cap: $7.52B. It is mid-cap and less subjective to small-cap rotation.

- Volume (last day): 11,758,780. Heavy traded.

- Tangible Book Value (3-Y average): -11.78%. It is a bigger decrease than TRTX’s -4.26%. But year-over-year is turning to a 13.96% increase for AGNC.

- Yield: 14.09%. It is a good dividend Capturer.

- Payout Ratio: 57.60%. It is a healthy payout ratio, indicating stable dividend distributions.

#3 Rithm Capital Corp. (RITM). The management has done a great job increasing the book value in the last 3 tough years. The dividend is a little lower than the double-digit yields. It is included in the current mREIT target group for the history of strong book values.

- Market Cap: $752.61M.

- Volume (last day): 1,190,814.

- Tangible Book Value (3-Y average): 5.08%. It is a very impressive book value appreciation over the 3 years, higher than the 5-year average of -4.48%.

- Yield: 8.61%. It is smaller than AGNC and TRTX.

- Payout Ratio: 45.66%.

#4 Blackstone Mortgage Trust (BXMT). BXMT’s shares have been hit pretty hard for its heavy office exposures. It is included here for the potential of a bigger recovery.

- Market Cap: $3.47B.

- Volume (last day): 2,141,039.

- Tangible Book Value (3-Y average): 2.20%. It is positive but a decline from the 5-year average of 3.80%.

- Yield: 12.59%. It is higher than TRTX and a good dividend Capturer.

- Payout Ratio: 85.22%.

Please keep in mind that the list in mREIT target group is a dynamic one. It will be updated with the continuous development of the mREIT market.

Risks and Caveats

One key risk of the investment thesis of this article is the US economy. Notice that the very reason for the Fed to firm its dovish rate bias is the slowing US economy. The recent PPI and unemployment numbers have offered some clues. I still believe that if the Federal Reserve cuts interest rates in a timely and appropriate manner, the so-called soft landing will be almost intact. But, of course, I cannot rule out the possibility of an economic recession. The fact that the yield curve still stays inverted is telling the market that we have not been completely out of the woods yet. The inverted curve will continue to have negative impacts on mortgages and mREITs. It could do more damage if the yield inversion would stay much longer.

As mentioned earlier, the dividend payout ratio is negative for TRTX. I believe the management is actively addressing it. The payout difficulty could certainly lead to the dividend cut if it is not improved soon enough.

Conclusion

Mortgage REITs are rebounding recently together with the equity REITs. The rally is expected to continue in the foreseeable future. Income investors want to take this opportunity to build mREIT positions in their portfolios. One way to do it is to use the WWE approach highlighted in the article. TRTX is recommended as a buy and used as a Core Engine with its small-cap growth potential. TRTX’s 10% dividend can also be used as an income Capturer, together with other mREITs highlighted, which are also offering double-digit yields.

Credit: Source link