: Why I Didn’t Buy The Tempting 13% Dividend Yield")

Thomas Faull

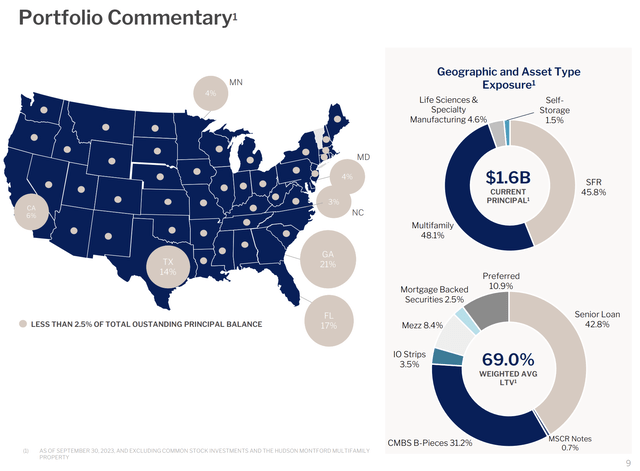

NexPoint Real Estate Finance (NYSE:NREF) last declared a quarterly base cash dividend of $0.50 per share, kept unchanged sequentially for a 13% annualized dividend yield. The mortgage REIT also declared a $0.185 per share special payment to become one of the only mREITs to pay out a special in a year that’s been mainly defined by disruption. Externally managed NREF is focused on originating and investing in a diversified mix of investments across several asset types. There was $1.6 billion in outstanding principal across 89 investments at the end of its third quarter including preferred equity, mortgage-backed securities, and first-lien mortgage loans. NREF has a heavy residential tilt with multifamily properties forming 48.1% of outstanding principal and single-family rentals forming 45.8% of its portfolio.

NREF Fiscal 2023 Third Quarter Supplemental

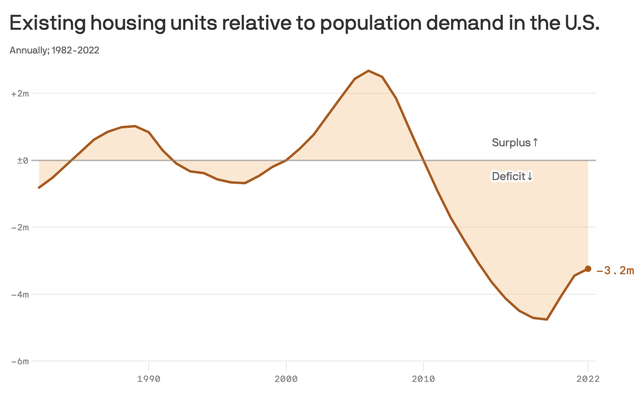

This aggregate 93.9% residential positioning forms an important hedge against rising office vacancy rates which has driven a markdown in the realized sales value of office properties. The AON Center, the third largest tower in Los Angeles, recently just sold for 45% below its 2014 sale price. Critically, mREITs like TPG RE Finance Trust (TRTX) which in 2021 had a 53% allocation to office-backed credit have realized elevated losses from the sale of loans and book value erosion. There is a US housing deficit of 3.2 million units as the economy and population continues to grow.

Axios

Hence, whilst there might be localized disruptions from oversupply, the national picture for multifamily and SFR housing is positive on a supply deficit that should support prices and continued construction. NREF is somewhat unique in that it has the highest SFR allocation versus its peers BXMT, STWD, and TRTX. Whilst this should inherently derisk its common shares, the mREIT has still realized a sustained decline in its book value.

Book Value And Cash Available For Distribution

NREF Fiscal 2023 Third Quarter Supplemental

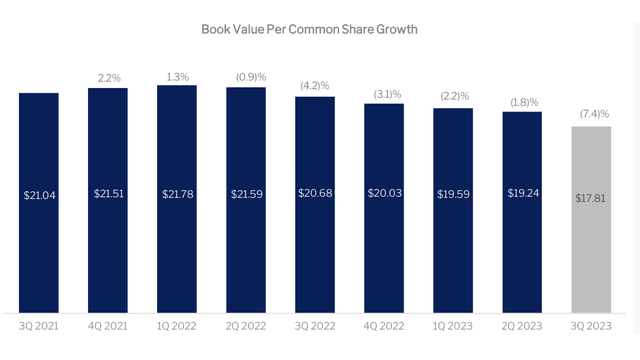

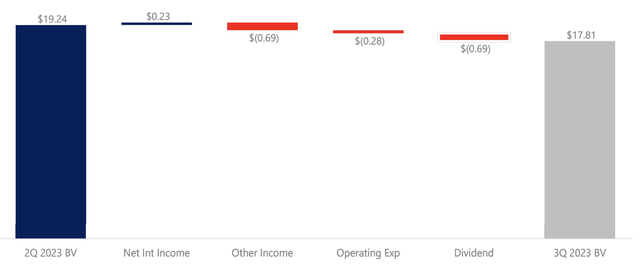

NREF’s book value was $17.81 per share at the end of its fiscal 2023 third quarter, a dip by $1.40 sequentially and by roughly 14% over its year-ago comp. There have now been six consecutive quarters of book value declining with the recent third quarter seeing the pace of this dip quicken with the 7.4% dip during the third quarter forming the largest sequential decline of book value since NREF went public. Not great.

NREF Fiscal 2023 Third Quarter Supplemental

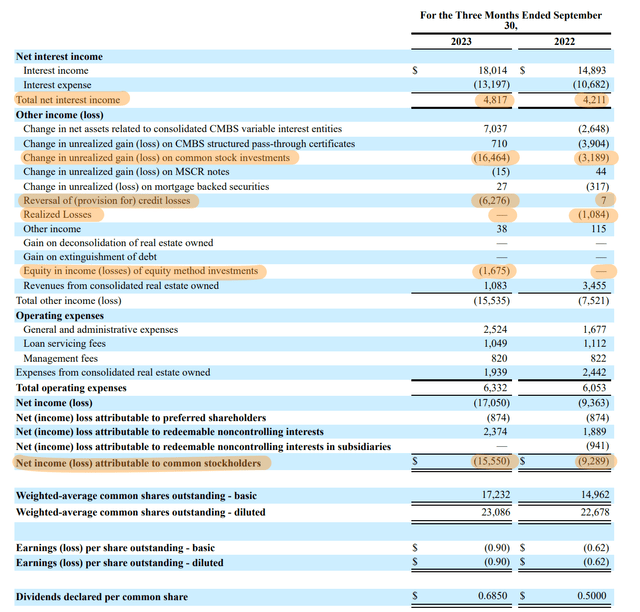

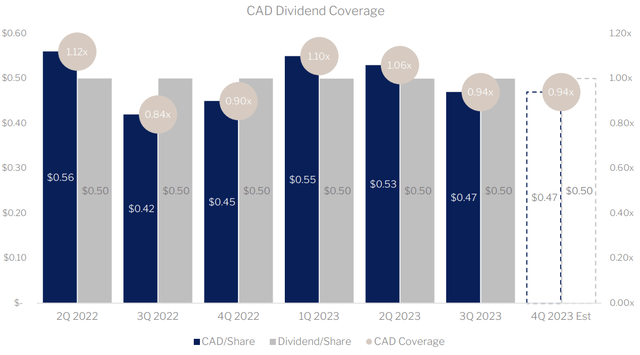

It reflects earnings for the third quarter that saw NREF report a net loss of $0.82 per share. This was up from a loss of $0.49 per share in the year-ago comp. NREF’s special dividend was essentially also paid out of book value with third-quarter cash available for distribution (“CAD”) at $0.47 per share. This meant NREF covered its base dividend by just 94%, a roughly 106% payout ratio. Including the special would see this payout ratio at 146%.

NREF Fiscal 2023 Third Quarter Form 10-Q

The loss during the period was driven by mark-to-market adjustments on common stock investments of $16.46 million and a higher provision for credit losses on a transition to CECL during the third quarter. Net interest income recorded a 14.3% year-over-year growth to $4.8 million, driven by originations of preferred equity investments with the overall portfolio with a weighted-average all-in yield of 6.90%, up 70 basis points from 6.20% in the year-ago comp.

NREF Fiscal 2023 Third Quarter Form 10-Q

Dividend Coverage And Underwriting Quality

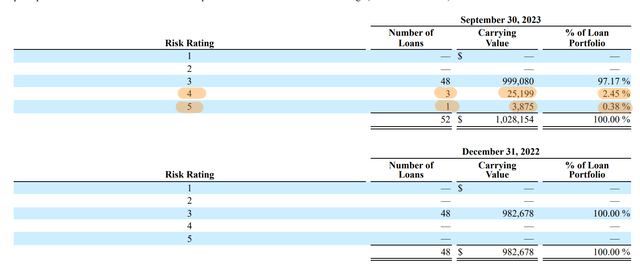

There were no loans in the portfolio in forbearance at the end of the third quarter with broader metrics of portfolio quality also somewhat flashing green. NREF’s weighted-average loan-to-value ratio stood at 69%, its debt service coverage was at 1.77x, and around 4 loans representing $29 million on principal saw their risk rating lowered. These 4 loans represented 2.83% of loans NREF classified as held-for-investment of $1.03 billion.

NREF Fiscal 2023 Third Quarter Form 10-Q

Hence, apart from the controversy surrounding the chairman of NREF’s board James Dondero, NREF is a defensively-minded mREIT with a residential-minded portfolio and a double-digit dividend yield. It’s important to flag that James Dondero once managed Highland Capital Management, a vehicle that invested in commercial credit backed by private equity, real estate, and unwanted life insurance policies. Highland filed for bankruptcy in 2019 and Dondero has twice been ruled in contempt of court in the ongoing bankruptcy court case.

NREF Fiscal 2023 Third Quarter Supplemental

The core stumbling block to a long position is the unsustainable dividend distributions. NREF is overpaying its dividend as CAD is insufficient to cover the distribution. This gap is set to continue in the fourth quarter with a further deterioration of book value almost certain. Hence, the current 13.4% discount to book value looks more like a liability than an opportunity with a possible dividend cut likely if NREF continues to not fully cover the distribution. The residential tilt of the portfolio and its use of preferred equity do render this a defensive ticker. Whilst I have no intention of building a position, this is a hold for existing investors.

Credit: Source link