Being organized is one of the keys to winning at the games we play, but I have to admit that I’d gotten lazy. When my wife and I recently counted up the number of currently-open credit cards we have, I was a bit surprised by the answer. We had fifty-three open cards. The cumulative in annual fees is staggering (though keep in mind that in some cases it is easier for someone like me to justify keeping a card given the fact that I write about credit cards and their benefits for a living). Still, I needed to create a plan of attack to reduce both the stress of tracking so many cards and the amount we’re paying in annual fees. The Platinum cards were a natural first target given their high annual fees.

Getting organized

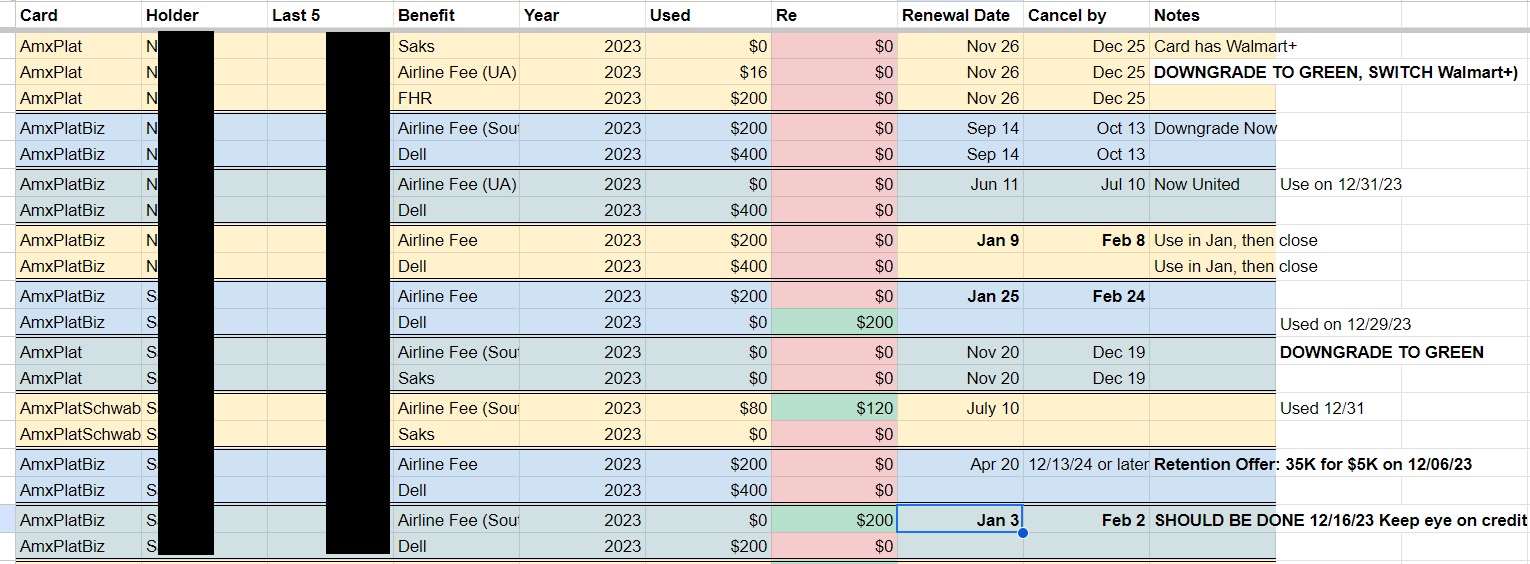

The first thing I did last month to reduce some of my mental stress was create a spreadsheet to track various “spoiling inventory” in the sense of annual credits, monthly credits, annual free night certificates, and other similar things across our cards. I created one tab just for Platinum cards that includes which of us holds the card, the last few digits of the card number, the key statement credit benefits and how much we have used / how much is remaining on each.

The sheet also has tabs for our Business Gold cards for their $20 monthly credits and for our free night certificates. I also created a tab for card-linked offers we should use where I’ll track Amex Offers that we should use or have used and that sort of thing.

That all helped make things visual and it has reduced the potential for mistakes in using, downgrading, or canceling the wrong card since I can see which credits are associated with which card, which airline has been chosen (I’ll probably break airline selection out into its own column), etc. I added a column for notes at the end where I could write reminders like the fact that I need to change our Walmart+ payment method before I get rid of the Platinum card currently associated with that charge.

Just before the end, there is a column with the date that the last annual fee was charged and a “cancel by” column to note the day about a month later that would be the approximate cancellation deadline (I didn’t figure those quite exactly at 30 days). My long-term plan is to get this entire sheet added to our normal monthly expense / budget-tracking spreadsheet, but I started it separately and haven’t yet perfected it. Still, it was instrumental in getting my stuff together. I’ll be the first to admit that I’m not a terribly good spreadsheet-maker, but I’ll also readily tell you that working for Frequent Miler has helped me realize just how useful a spreadsheet can be.

I should add that Platinum cards have additional benefits like the Uber credits and digital entertainment credits that aren’t shown here. That’s because I end up using all of our Uber credits on a single dinner order once a month, so I don’t need individual tracking for those, and I don’t currently use the digital entertainment credits (my mistake on forgetting to change my Disney+ membership to monthly before it renewed at the annual rate!). I just don’t use the rest of the qualifying services at all.

Our Amex consumer Platinum card plan of attack

My wife and I currently have 3 consumer Platinum cards and six Business Platinum cards between us. That’s far too much Platinum at a $695 annual fee for each.

We have a Schwab Platinum card, which we keep for times when we decide to cash out points given that you can redeem points for a deposit to your brokerage account at a value of 1.1c per point. We also each have a regular “vanilla” Platinum card that we opened under incredible welcome offers during the pandemic (you may recall that I bought a car and earned over half a million points). We kept those consumer Platinum cards because Amex has targeted subsequent new cardmember referral offers to some customers and we have each had a turn or two where one of these cards has referred to the best available Platinum card offer, so we’ve each maxed out our referral points on these cards for the past couple of years.

We’ve made decent use of the benefits on these cards: we had no trouble using our Fine Hotels & Resorts / The Hotel Collection benefits (last year, we ended up using those during our extended stay in Las Vegas and we used credits from the previous year for a stay in Brussels, Belgium over the summer). We used our Uber credits for Uber Eats in every month but one and we used our airline incidental credits between United and Southwest as outlined in our post about Amex airline fee reimbursements: What still works?. While I wouldn’t value those benefits at face value, when combined with the referral points earned from each card, the math has made them worth keeping.

At least, that was true until I looked at a spreadsheet with 53 active credit cards, 9 of which are Platinum cards. The calculus has changed on that as we haven’t had referral offers at all on our consumer Platinum cards recently and I know that we will still likely have opportunities to pick up some referral points with other cards. I decided that we each need to drop a consumer Platinum card.

The 30-day window missed: downgrading for a pro-rated annual fee

My wife and I each had a consumer Platinum card that renewed in late November. We had until late last month to cancel without having to pay the annual fee. Unfortunately, I left our airline incidental credits until late in the year to use up. As fate would have it, the credits posted one day after the 30-day mark from the date the annual fee charged, so we couldn’t avoid paying the new annual fees entirely. If we canceled those cards more than 30 days from the date the annual fee posted, we wouldn’t get anything back — we’d have just lit $695 on fire (times two!).

However, the fact that the credits were slow in posting is only a small bummer since the airline incidental fee credits and Fine Hotels & Resorts / Hotel Collection credits are calendar year benefits. By holding these cards an extra couple of weeks beyond when we intended to cancel them, we’ll get a chance to each use our $200 Fine Hotels & Resorts credit for 2024 and our $200 airline incidentals benefit for 2024. I haven’t yet seen something that strikes my fancy at Saks Fifth Avenue, but we have a trip coming up this month that will put us in the vicinity of a Saks store, so we’ll probably each buy a $50 gift card in-store to use the January-to-June Saks benefit. To be clear, that credit is not supposed to work for gift cards, but in practice gift card purchases made in-store have credited like any other purchase.

Once the credits for all of those purchases post, we’ll each downgrade to a consumer Green card. Because we are beyond the 30-day window since the annual fee was charged, Amex will no longer refund the annual fee in full. However, they will pro-rate the annual fee if we downgrade. Therefore, we’ll both look to downgrade to a consumer Amex Green card. When we do, I expect that we’ll each get refunded about $580 and then get charged about $125 for the prorated Green card annual fee (I’m assuming that we’ll get charged for 2 months of Platinum card membership and 10 months of Green card membership).

A need for Green before we downgrade

Neither of us have ever had the consumer Green card. That presents a further wrinkle: Amex application terms indicate that you can not get the welcome bonus on a card that you have or have had previously. Therefore, if we downgrade our Platinum cards to Green cards, we will not be eligible for welcome bonuses on the Green cards in the future.

While neither of us are excited about the current Green card welcome offer at the time of writing, we each have at least one current Amex card offering 20,000 Membership Rewards points per referral. Keep in mind that Amex allows cross-referrals, so if my Business Gold card shows a bonus of 20,000 Membership Rewards points when a friend is approved, I can create a referral link from my Business Gold card to refer my wife to a consumer Green card. See more details and a video explaining this in more detail in this post: How to create cross-brand Amex referrals.

That means that if I refer my wife, she’ll get the current Green card welcome offer and I’ll get 20,000 points when she is approved. The same is true the other way — she can refer me and earn 20,000 points on top of the welcome offer that I earn. Between the two of us, that’s like a bonus third welcome offer for both opening the Green card with each other’s referral links. While Amex family language prevents those who have or have had a Platinum card from getting a Gold card, there is no such family language on the Green card at the time of writing.

Again, the current welcome offer on the Green card is low. I wish we could wait for a better welcome offer (or that we had jumped on a better offer over the last couple of years!). However, given that we each want to downgrade a Platinum card imminently, the time is now for us each to get a Green card with a welcome bonus. Maybe I’ll give it a few more days or a week just in case the offer changes, but I’ve got no reason to expect that it will in the near-term.

That means that we’ll end up paying either a prorated or new annual fee on four Green cards between the two of us, but we’ll still spend at least $700 less than we would have if we kept the Platinum cards. And by each opening the Green card for a welcome bonus before downgrading a Platinum card, we’ll end up with 120,000 points between welcome offers and referral points. We’ll also trigger $400 in airline incidental credits, $400 in Fine Hotels & Resorts credits, and we’ll “bank” $100 in Saks credits between the two of us with our Platinum cards before downgrading. I imagine we’ll also each use our $15 Uber credits this month via Uber Eats. After a year has passed, we’ll likely both intend to cancel the Green cards we got by downgrading Platinum cards and we’ll likely look for a retention offer on our new Green cards to make them worth keeping.

That will take care of two consumer Platinum cards. We’ll keep the Schwab Platinum. But what about all those Business Platinum cards?

Amex Business Platinum plan

On the Business Platinum side, we each have three Business Platinum cards that we’ve gotten thanks to Amex’s repeated targeted “expand your membership” offers to open new Business Platinum cards without lifetime language. I like the idea of each of us keeping a Business Platinum card thanks to the 35% Pay-with-points rebate. While we haven’t used that extensively, we’ve used it at least once a year each of the past several years (most recently just last week to book flights on Spirit Airlines after our holiday plans went haywire). Still, we don’t need the six cards we currently have. While some will find it useful to have more than one Business Platinum in order to set them up with different airlines for the rebate on economy class flights, I’ve had no trouble changing my airline even after having partially used the airline fee credit, so I’ll just plan to hold one card each for the rebate.

Each of us has one Business Platinum card set to renew within the next few days, so these will be easy to handle. We’ll look to each use our $200 in airline incidental benefits and the $200 Dell credit for January-June within the next week and then we’ll cancel these cards before the annual fee comes due next month (within 30 days of the date the fee is charged). That will drop us to four Business Platinum cards (which is still too many!).

We have another Business Platinum card where the annual fee will come due late next month. We’ll likely also look to use the benefits on that card one more time and then cancel it outright as soon as the annual fee is charged. And then there were three . . .

Last month, my wife tried to cancel one of her Business Platinum cards. That card had renewed all the way back in April. While it wouldn’t have made a ton of sense to cancel right before calendar-year credits renewed in January, we were looking to make progress toward the goal of fewer cards and had decided to sacrifice the shot at one more round of credits in favor of getting one card off the chopping block. She chatted with support to cancel and to my surprise, she was given a retention offer of 35,000 points with $5,000 in purchases. That’s effectively 7 additional points per dollar over the 1 point per dollar that the card ordinarily earns on most purchases. If you assume that we would have ordinarily earned at least 2 points per dollar on that $5K in purchases if we had put the purchases on a different card, you could account for it really feeling like an additional 6 points per dollar spent. That was enough to make it worth keeping that Business Platinum card since we have enough in ordinary expenses to meet the spend without sacrificing anything else. That leaves us with two more Business Platinum cards to deal with.

Our last two Business Platinum cards are set to renew later in the year — one in June and the other in September. I’d like to keep one open for future 35% rebates, but I don’t need both cards. Therefore, I intend to use the airline fee credits and Dell credits right away on the card set to renew in September and then I will downgrade that card to a Business Green card as soon as possible, intending to cancel it when it comes up for renewal next September. The reason I’ll look to downgrade that card ahead of the other one is because it has been used for three fewer months, so I expect to get an additional ~$175 back when I downgrade that card over what I would get for the card set to renew in June.

Here’s what I mean:

- The card with a June anniversary date is now 7 months into the cardmember year. If I downgraded today, I would expect to get a prorated refund for 5 months of the $695 annual fee (5/12 of $695 is about $289).

- The card with a September anniversary date is now 4 months into the cardmember year. If I downgraded today, I would expect to get a prorated refund for 8 months of the $695 annual fee (8/12 of $695 is $396.67).

In short, I’ll get an additional $100+ back if I downgrade the card with the later anniversary date. I’m still not getting a remarkable deal since I’ve already long ago paid the annual fees, but I’d rather get an extra hundred bucks back than not get it back.

I won’t look for a retention offer right now on whichever card I close because that would lock me into keeping the card for another 13 months — meaning that I’d be stuck in another mid-year downgrade/cancel crisis 13 months from now. I’d rather just clean up the mess.

The points parade has been a lot of fun, but now it’s getting expensive and I need to make sure that I get off the hamster wheel before it takes me for a ride.

Bottom line

After carrying out the plans laid above, we’ll each have one Business Platinum card and my wife will also have a Schwab Platinum card – reducing our Platinum portfolio from 9 Platinum cards to 3. That’s a pretty significant savings that makes a nice dent in our cumulative annual fee outlay. I still have plenty of work to do to thin the herd of credit cards in our stable before the fees thin our savings more than we’d like, but these Platinum plans are important to handle sooner rather than later so that we can take advantage of calendar year benefits without stretching the downgrade and cancellation process farther than necessary since time definitely equals money in fees we’ll be charged or lose. In the future, I hope that my new spreadsheet will keep me a bit more organized so that I’m not scrambling with 30-day deadlines at the end of a cancellation window and we can be sure to avoid letting any benefits go unused. Again, organization is a major key to winning the games we play.

Want to learn more about miles and points? Subscribe to email updates or check out our podcast on your favorite podcast platform.

Credit: Source link