Household expenses are on the rise, causing growing financial stress for many Americans. In 2022, the Bureau of Labor Statistics found that the average household spent an average of $72,967 on common expenses, ranging from housing to childcare to utilities.

However, some expenses can lead to more anxiety and frustration than others. We surveyed Americans across different age groups to determine the most troublesome costs and provide expert tips on managing your monthly bills.

Key points

Here’s what we learned from our study on everyday expenses Americans hate the most:

- 71% of Americans say they’re stressed by their ability to afford everyday expenses.

- Americans most regularly spend money on groceries, phone bills, utilities, gasoline and rent/mortgage payments.

- Grocery bills frustrate Americans more than any other regular expense. Utilities, rent/mortgage payments, gasoline and insurance payments round out the top five most annoying expenses.

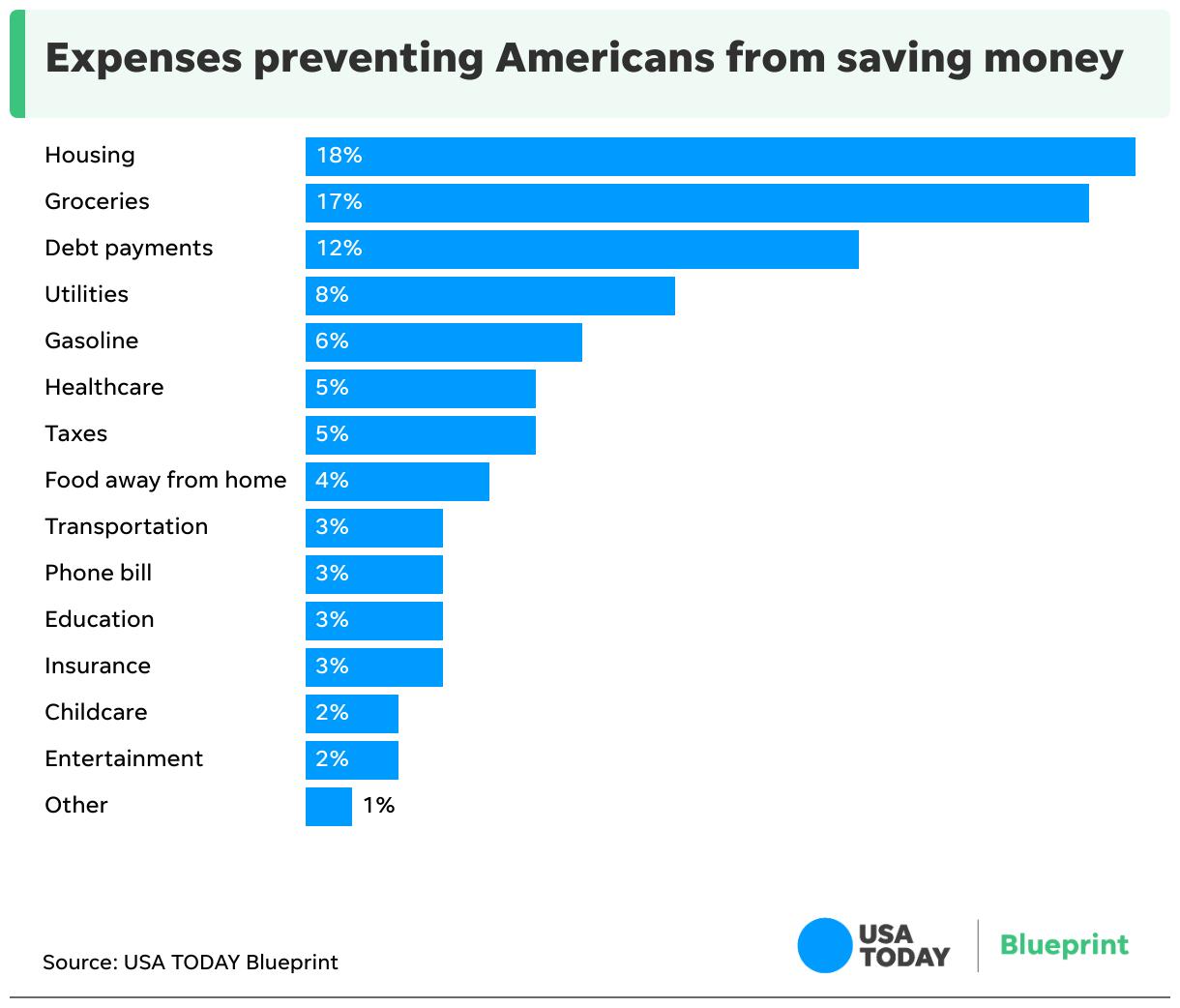

- Shelter, food and…debt? Americans say housing costs, groceries and debt payments have the biggest impact on their ability to save money.

This online survey of 2,000 general population Americans was commissioned by USA Today Blueprint and conducted by market research company Talker Research, in accordance with the Market Research Society’s code of conduct. Data was collected from March 29 to April 4, 2024. The margin of error is +/- 2.2 points with 95% confidence. This survey was overseen by Talker Research, which is made up of members of the Market Research Society (MRS) and the European Society for Opinion and Marketing Research (ESOMAR).

Data from the Silent Generation (born between 1928 and 1945) was included in the overall analysis, but due to the limited sample size, it was excluded from generational comparisons.

The impact of American expenses

Before diving into the results, we wanted to examine the biggest spending categories for American households. According to data from the Bureau of Labor Statistics, the top three annual expenses for the average American household in 2022 (the most recent data available) were housing (33.3%), transportation (16.8%) and food (12.8%).

For most Americans, spending money in these areas is unavoidable. Our survey revealed that Americans are notably frustrated with where their money is going but that it doesn’t always correspond with the biggest financial burdens. Most Americans surveyed responded that they’re also stressed about personal finances and the difficulty of saving money. Let’s take a closer look at the most frustrating expenses and who is feeling the strain the most.

Expenses that frustrate Americans the most

We polled households to identify the most annoying monthly expenses for Americans. Although housing is by far the largest expense, it isn’t necessarily the monthly cost that bothers Americans the most. Across all age groups surveyed, groceries were the most frustrating expense, even surpassing transportation and housing, which easily cost Americans more annually.

Case in point: the average consumer household spent over $5,700 on “food at home” in 2022 compared to spending over $12,000 on transportation. Yet, 40% of respondents cited groceries as their most frustrating expense, while only 8% felt the same about transportation. The primary reasons for this annoyance were the high cost of groceries and significant price increases due to inflation.

Interestingly, while most Americans are annoyed by the same expenses, the reasons tend to vary by generation. More than two-thirds (70%) of baby boomers surveyed responded that costs are too high or prices have increased too much. While these factors also bother younger generations, Gen Z and millennials were more likely to cite a lack of control in costs (23%), that they’re unfair or unequal (15% and 13%, respectively) or that it’s difficult to understand how prices are formulated (15% and 14%, respectively).

Regular expenses are chipping away at American savings

Monthly bills aren’t just annoying — they’re significantly eroding households’ ability to save money. However, the specific expenses that affect Americans’ savings (and average debt) will vary greatly depending on their age group. In the survey, we found that housing costs are the biggest obstacles to saving money for younger generations, while older generations are most affected by their monthly grocery expenses.

Financial stress levels are highest among millennials (77%), followed by Generation Z (75%) and Generation X (74%). Baby boomers reported experiencing the least financial stress, although at 59% it was still more than half of those surveyed.

Managing their finances frustrates the majority of Americans

Beyond specific expenses, simply managing finances can be a major source of frustration. Over half of all respondents (56%) reported frustration with staying on top of personal finances. From credit cards to bank accounts to student loans, it can seem like an impossible balancing act to oversee accounts and keep track of expenses, let alone save for the future.

Women reported more frustration with financial management than men (62% vs. 49%) as well as higher levels of stress about affording everyday expenses (76% vs. 67%). More than half of younger Americans are feeling the strain of staying on top of their finances — Gen Z (62%), millennials (59%) and Gen X (60%) — while only 43% of baby boomers said the same.

Baby boomers were the least frustrated by bank accounts (5% vs. 14% average), suggesting that more established financial accounts or existing bank relationships can reduce the stress of financial management. They’re also less likely to be feeling the burden of loans, such as student loans. That said, baby boomers reported being much more frustrated by credit cards than any other generation (45% vs. 28% average).

How to save on everyday expenses with cash-back credit cards

Whether you want to save on everyday expenses or pay down your debt, it’s important to assess what you’ve got in your wallet. While applying for a new credit card may seem counterintuitive, you could boost your credit score and even earn valuable rewards.

The key is to know how to manage credit cards effectively. Before applying, you should be aware of the annual percentage rate (APR) for purchases and balance transfers. It’s also important to feel confident in your ability to pay the entire billing statement by the monthly due date. Otherwise, you could face serious interest and late charges that can easily pile you with debt.

The best cash-back credit cards offer everyday rewards without incurring an annual fee. These types of credit cards offer a set amount of cash back on all purchases or offer elevated rewards on bonus categories, such as groceries or gas. Here’s an overview of some of our favorites:

Ultimately, the best credit card for you will provide powerful rewards that are well-suited to your spending habits. You can redeem those hard-earned rewards for cash back in your pocket, which can help you save money on groceries and reduce your living expenses.

How to get a cash-back credit card

Once you’re ready to take that leap, there are a few necessary steps to take before applying. For starters, you’ll want to check your credit score to know your approval odds, as many rewards credit cards require a good to excellent credit score. Remember that many factors, such as your credit utilization ratio, go into determining your credit score.

When applying, you’ll have to provide your Social Security number (SSN) and income level, among other information. Many issuers will provide instant approval to those who qualify, while others may have to provide more documentation to support their application.

That said, if your credit score isn’t quite up to snuff — perhaps it falls around the poor to average range — you may want to consider a secured card that can help you rebuild your credit. They’re easier to qualify for because they require a cash deposit that typically defines your monthly credit limit.

No matter which credit card you end up with, building that on-time payment history will be the secret sauce to improve your credit score over time.

For rates and fees for the Blue Cash Preferred® Card from American Express please visit this page.

Credit: Source link